Agentic Innovation Economics: Autonomous AI Agents and the Future of Endogenous Technological Change

This paper introduces Agentic Innovation Economics (AIE), a formal theoretical framework that extends classical endogenous growth theory to accommodate the emergence of autonomous AI agents as productive innovators rather than merely productivity-enhancing tools. Building on the Romer–Jones knowledge-production tradition, we construct a three-sector model in which knowledge accumulates according to a hybrid dynamics equation incorporating a superlinear agentic exploration term. We derive the balanced growth path and establish that agentic R&D generates supra-Romer endogenous growth when the AI scaling exponent exceeds a critical threshold. Four testable propositions are formalised and linked to the emerging empirical literature.

Abstract

This paper introduces Agentic Innovation Economics (AIE), a formal theoretical framework that extends classical endogenous growth theory to accommodate the emergence of autonomous AI agents as productive innovators rather than merely productivity-enhancing tools. Building on the Romer–Jones knowledge-production tradition and the emerging literature on AI as a general-purpose technology (Brynjolfsson et al., 2021; Truong & Papagiannidis, 2022), we construct a three-sector model—Final Goods, Human R&D, and Agentic R&D—in which knowledge accumulates according to a hybrid dynamics equation incorporating a superlinear agentic exploration term. We derive the model’s balanced growth path (BGP) and establish that agentic R&D generates supra-Romer endogenous growth when the AI scaling exponent satisfies \gamma > 1/(1-\phi), where \phi is the knowledge-stock complementarity parameter. We characterise the transition between human-bounded and agent-driven innovation regimes, derive the firm-level optimal investment in human researchers versus AI agents, and identify the winner-take-most equilibrium arising under compute-capital concentration. Four testable propositions are formalised and linked to the emerging empirical literature on AI firm-level growth, skill-based labour demand, and automation’s task-displacement effects. We demonstrate that human and agentic R&D inputs are technological complements in the medium run even as they become substitutes at the task level—a bifurcation with profound implications for labour market policy. We conclude with an integrated governance framework addressing compute monopoly, responsible AI in knowledge creation, decentralised autonomous innovation structures, and the allocation of agentic innovation rents, offering concrete policy prescriptions grounded in our formal model. The paper speaks directly to the technological forecasting agenda by identifying the parametric conditions under which a regime shift from incremental to accelerating innovation occurs, and to the social-change agenda by tracing how compute concentration translates into innovation inequality, declining labour income shares, and governance challenges for the algorithmic economy.

Keywords: Agentic AI; endogenous growth; knowledge production function; autonomous agents; computational capital; innovation economics; AI governance; Schumpeterian dynamics; general-purpose technology; decentralised autonomous organisations.

JEL Codes: O31, O33, O41, L11, D83, E25.

1. Introduction

For more than three decades, economists have understood technological change as an endogenous outcome of purposeful investment by human researchers, operating within a market environment that balances the public-good character of ideas against the private incentives created by temporary monopoly rents (Aghion & Howitt, 1992; Jones, 1995; Romer, 1990). In these canonical frameworks, knowledge is non-rival and accumulated through deliberate human-directed R&D: the engine of long-run growth is, ultimately, bounded by human cognitive capacity and the number of researchers.

A profound shift is now underway. Systems of autonomous artificial intelligence agents—capable of formulating hypotheses, executing experiments in digital environments, iterating over solution spaces, and coordinating with other agents without continuous human supervision—are being deployed at scale across R&D laboratories, pharmaceutical pipelines, software development platforms, and scientific research workflows (Al-Hamad et al., 2025; Ante, 2026; Prokopowicz et al., 2025; Xiong et al., 2025). The “AI Scientist” project (Al-Hamad et al., 2025) provides the most vivid instance: a fully autonomous pipeline generating, reviewing, and publishing scientific research with minimal human involvement. Agentic systems such as AutoGPT, CrewAI, and AutoGen are entering enterprise R&D workflows (Haefner et al., 2021), while foundation-model providers now train on compute budgets that dwarf the capabilities of any single academic institution (Vipra & Korinek, 2024). These developments demand a new theoretical language.

The transformative character of this shift is underscored by the economics of general-purpose technologies (GPTs). Brynjolfsson et al. (2021) document that the adoption of GPTs such as information technology is accompanied by a “productivity J-curve,” wherein short-run disruption precedes long-run acceleration as complementary innovations and organisational adaptations accumulate. AI, and especially agentic AI, is increasingly recognised as the defining GPT of the current era (Cockburn et al., 2019; Truong & Papagiannidis, 2022). What distinguishes agentic AI from prior GPTs, however, is its capacity to accelerate its own adoption trajectory—AI agents can themselves perform the complementary innovation and organisational adaptation work that GPT diffusion requires, potentially compressing the J-curve. This self-referential feature of agentic innovation is the central concern of the present paper.

The present paper develops a formal theoretical language for this challenge. We introduce Agentic Innovation Economics (AIE), defined as the sub-field of innovation economics concerned with the conditions under which autonomous AI agents function as productive economic actors in the knowledge-creation process, and the macroeconomic and societal implications of agent-driven discovery. Our framework makes four central contributions.

First, we extend the Romer–Jones knowledge-production function to incorporate a hybrid human–agentic R&D sector, where agentic output exhibits superlinear scaling in the number of agents A (through parallel exploration and self-improvement loops), governed by parameter \gamma. We derive the balanced growth path (BGP) and show that when \gamma > 1/(1-\phi)—where \phi is the knowledge-stock complementarity coefficient—the model delivers supra-Romer growth: a permanent acceleration in the idea production rate analogous to the Type~I singularity of Aghion et al. (2019), but arising from agent scaling rather than full task automation.

Second, we develop a firm-level model in which profit-maximising firms choose between human researchers H and AI agents A subject to a wage w and compute cost c. We characterise the optimal input mix, identify the compute-cost threshold below which firms entirely substitute agents for human researchers in exploratory R&D, and derive the welfare and distributional implications of this substitution. Consistent with the information-processing hierarchy of Haefner et al. (2021), we show that human and agentic R&D are technological complements at the level of the innovation system even as they substitute at the task level.

Third, we formalise four testable propositions linking the model’s predictions to measurable empirical outcomes—firm-level product innovation, R&D labour demand, industry concentration, and knowledge ownership—and discuss how existing evidence (Acemoglu & Restrepo, 2019; Babina et al., 2024; Besiroglu et al., 2024; Bone et al., 2025; L. Huang et al., 2025) bears on each.

Fourth, we develop an integrated governance architecture addressing compute infrastructure policy, responsible AI in knowledge creation (Dai et al., 2026), decentralised autonomous innovation governance (Santana & Albareda, 2022), and the allocation of agentic innovation rents. The governance analysis is grounded in the formal model’s welfare implications rather than being a descriptive addendum.

This paper speaks directly to both dimensions of Technological Forecasting and Social Change: to the forecasting agenda by identifying the parametric thresholds (\gamma > 1/(1-\phi)) that determine when the innovation regime shifts from incremental improvement to accelerating discovery; and to the social-change agenda by tracing how compute concentration, agentic labour substitution, and autonomous governance structures translate theoretical model predictions into distributional and institutional consequences.

The remainder of the paper is structured as follows. Section 3 surveys the four literatures we draw upon, incorporating the rapidly growing body of TFSC-published research on AI and innovation. Section 4 presents the formal AIE model and derives its BGP. Section 5 develops the firm-level investment problem. Section 6 analyses market structure effects and compute-capital concentration. Section 7 discusses labour market implications, including skilled-labour complementarity and the skill-based hiring transition. Section 8 draws the governance and policy implications. Section 9 identifies empirical research designs. Section 10 addresses limitations. Section 11 concludes. Formal proofs are in the Appendix.

2. Literature Review

2.1 Endogenous Growth Theory: The Romer–Jones Tradition

The theoretical foundations of AIE rest on the endogenous growth literature initiated by Romer (1990). Romer’s central insight—that ideas are non-rival, that their production exhibits increasing returns to scale, and that imperfect competition is therefore necessary to sustain R&D investment—remains the bedrock of our framework. In the Romer model, knowledge accumulation follows \dot{A} = \delta H_A A, where H_A is the human capital employed in R&D and \delta is research productivity; this linear-in-researchers specification implies that growth rates are an increasing function of the research workforce size, generating the contested “scale effect” (Jones, 1995).

Jones (1995) addressed the empirical failure of the scale effect by introducing diminishing returns to the existing knowledge stock in idea production, yielding the semi-endogenous specification \dot{A} = \delta H_A^\lambda A^\phi with \phi < 1 and \lambda \leq 1. Jones demonstrated that this framework generates steady-state per capita growth driven by population growth rather than by the number of researchers, reconciling the model with the absence of accelerating growth despite a rising share of scientists in OECD economies (Bloom et al., 2020; Jones, 2021).

Subsequent work extended the framework in several directions: Aghion & Howitt (1992) introduced quality ladders and creative destruction; Grossman & Helpman (1991) developed the variety-expansion model; and Acemoglu & Restrepo (2018) introduced a task-based model in which research can be directed toward automation (replacing existing tasks) or the creation of new tasks, with implications for factor shares and employment. A critical contribution for the present paper is Aghion et al. (2019), who analyse the macroeconomic conditions under which AI may cause explosive growth, showing that a singularity requires the automation of tasks involved in the production of ideas themselves. Jones (2024) extends this analysis to characterise transitional dynamics under transformative AI, providing the most comprehensive treatment of AI’s growth implications to date within the endogenous growth framework.

2.2 AI as a General-Purpose Technology and Innovation Enabler

A fundamental insight for situating AI within innovation economics is its character as a general-purpose technology (Brynjolfsson et al., 2021). GPTs share three characteristics: pervasiveness, improvement over time, and the capacity to spawn complementary innovations. Truong & Papagiannidis (2022) provide systematic evidence that AI functions as a GPT by enabling innovation across four distinct stages—discovery, screening, experimentation, and development—reducing uncertainty and lowering the cost of laborious cognitive tasks at each stage. This positions AI not merely as a productivity tool but as a structural modifier of the innovation production function itself.

Haefner et al. (2021) develop a three-level information processing capability framework that distinguishes AI’s role as (i) Exploiting existing knowledge (pattern recognition, optimisation within known problem spaces), (ii) Expanding knowledge boundaries (recombination, analogy, anomaly detection), and (iii) Exploring unknown territories (hypothesis generation, open-ended search). This hierarchy is directly relevant to the AIE model: the agentic R&D sector in our framework operates primarily at the Exploring level, whereas human-AI collaborative R&D spans all three levels. The behavioural theory of the firm (Cyert & March, 1963) grounds this framework in bounded rationality and information processing constraints that AI agents are progressively overcoming (Haefner et al., 2021).

Bahoo et al. (2023) provide the most comprehensive systematic review of AI in corporate innovation to date, synthesising 364 articles spanning 1966–2022 across eight focal research streams. Their review establishes that AI fundamentally redesigns corporate innovation processes rather than merely accelerating existing ones, with implications for competitive dynamics, organisational structures, and the distribution of innovation rents. This finding is consistent with AIE’s central claim that agentic AI qualitatively changes the innovation production function.

2.3 AI-Augmented R&D and the Ideas Production Function

A growing empirical literature documents the effects of AI on scientific productivity and innovation. Besiroglu et al. (2024) present an endogenous growth analysis of deep learning as a capital-deepening technology in R&D, providing estimates of the deep-learning idea production function from computer vision tasks and concluding that if deep learning diffuses widely, the US economic growth rate may double. Agrawal et al. (2019) argue that AI fundamentally alters the economy’s knowledge production function, distinguishing between AI’s effects on the output production function (modest long-run growth implications) and its effects on the knowledge production function (potentially transformational).

Naude (2024) propose three models of AI in the ideas production function—AI as research-augmenting technology, AI as researcher scale-enhancing technology, and AI as innovation facilitator—showing through model simulations calibrated to US data that an economic growth explosion from AI alone would require specific and perhaps unlikely parameter combinations. Gans (2025) model AI as a system that enables interpolation between known knowledge points, deriving a threshold AI capability level above which the direction of research shifts from incremental improvement to frontier exploration, with consequences for the long-run growth rate.

K. G. Huang et al. (2025) develop a three-level pyramidal framework for breakthrough innovations in which AI serves as a key enabling technology: (i) exploring and identifying breakthrough opportunities, (ii) analysing and managing innovation ecosystems, and (iii) synthesising and strategising via digital platforms. Their framework corroborates AIE’s three-sector architecture by identifying AI agents as operating distinctively across all three levels of the innovation pyramid, with qualitatively different knowledge production functions at each level.

At the firm level, Babina et al. (2024) provide the most comprehensive empirical evidence to date, using a novel resume-based measure of firm-level AI investments for 64% of the US workforce and documenting that AI-investing firms experience significantly higher growth in sales, employment, and market valuations, driven primarily through increased product innovation rather than cost reduction. This result supports our model’s prediction that agentic R&D affects growth primarily through the knowledge production function rather than through direct goods-sector productivity.

2.4 Autonomous AI Agents as Economic Actors

The specific contribution of AIE—treating AI agents as economic actors rather than capital goods—draws on a rapidly developing literature on agentic systems. Prokopowicz et al. (2025) document the emergence of agentic AI in 2024–2025 as a paradigm shift from passive generative models to systems with “mechanisms of autonomy, long-term memory, multi-stage planning, and interaction with the environment,” arguing that such systems constitute active participants in decision-making rather than tools. Al-Hamad et al. (2025) systematically review how agentic AI enables autonomous decision-making and process automation, highlighting the transition from “Copilot” (assisted) to “Autopilot” (autonomous) operational models in enterprise R&D.

Ante (2026) provide the first comprehensive empirical mapping of autonomous AI agents as economic actors, analysing 306 AI agents operating in decentralised finance (DeFi) ecosystems. Their typology identifies four categories—Trading & Analytics, Development & Infrastructure, Sentiment & Community, and Entertainment & Engagement—and shows that these agents actively reshape market coordination, governance structures, and organisational architectures. The study documents an aggregate market capitalisation of $8.6 billion for AI agent-related tokens as of December 2024, confirming that agentic AI systems are already functioning as autonomous economic actors at meaningful scale. Critically, Ante (2026) develop a governance framework mapping AI agents across autonomy and decentralisation dimensions, demonstrating that the critical trade-offs between efficiency, transparency, and control identified in our theoretical model manifest empirically in DeFi market structures.

Arsenyan et al. (2023) develop a human–virtual agent coexistence framework encompassing 16 topics across four dimensions: interaction context, agent characteristics, human–agent interactions, and application domains. Their conceptual synthesis positions “coexistence” as a broader and more appropriate frame than “interaction,” capturing the sustained, multi-domain, bidirectional relationship between human and artificial agents. This framework directly supports AIE’s treatment of human researchers and AI agents as co-participants in the innovation production system—neither purely complementary nor purely substitutable, but functionally interdependent across the innovation pipeline.

The economic significance of this shift is emphasised by Xiong et al. (2025), who document that agentic systems can execute not just routine but complex cognitive tasks, potentially automating multi-step research workflows that previously required sustained human expertise. This parallels Schumpeter’s original insight about the role of the entrepreneur as the engine of economic dynamics (Schumpeter, 1942): AIE asks whether, and under what conditions, AI agents can perform the Schumpeterian entrepreneurial function of combining existing knowledge in novel, economically productive ways.

2.5 Labour Market Effects and Distributional Consequences

Our model’s labour market implications are situated within the task-based framework of Acemoglu & Restrepo (2019), who decompose the effects of automation technology on labour demand into a productivity effect (AI raises total output, increasing demand for all factors) and a displacement effect (AI substitutes for labour in specific tasks, reducing labour demand). They show that the net effect on employment depends on the balance of these two forces, and that automation is associated empirically with declining labour income shares.

Bone et al. (2025) provide the most direct empirical evidence on the labour market transformation driven by AI adoption, documenting that skill-based hiring for AI roles commands a 23% wage premium exceeding the premium for doctoral credentials (33%), that demand for AI roles grew 21% over 2018–2023 while degree requirements for these roles dropped 15%, and that AI adoption is reshaping the labour market structure around competency rather than credentialing. This evidence is directly consistent with AIE’s prediction (Proposition 6) that agentic innovation creates bifurcated labour markets in which demand rises for highly skilled “agentic supervisors” and falls for routine exploratory R&D workers.

L. Huang et al. (2025) provide panel evidence from 935 Chinese manufacturing firms (2010–2022) that AI technology adoption facilitates human and structural capital for value creation, with the boundary between AI and human intelligence lying at the level of cognition and creativity where AI is currently “semi-cognitive.” Their finding that AI augments rather than replaces human intelligence in the medium run provides empirical grounding for AIE’s human–agent complementarity thesis in the transitional dynamic before full agentic capability is achieved.

Lowitzsch et al. (2024) extend the automation analysis to the long-run distributional consequences, documenting the accelerating transfer of income from labour to capital owners under AI-driven automation. Lu (2021) provide a three-sector endogenous growth model incorporating AI’s self-accumulation ability and its non-rival character, showing that AI development raises growth along the transitional dynamics path but may be detrimental to household welfare when firms substitute AI for labour rather than augmenting it.

The concentration dimension is examined by Vipra & Korinek (2024), who document that foundation model development is dominated by a small number of firms spending tens of billions on GPU infrastructure, a market structure that exhibits near-monopoly characteristics in key segments (Rikap, 2024). This is directly relevant to AIE’s prediction that compute-capital concentration can create winner-take-most dynamics in agentic innovation, reinforcing the case for policy intervention (Narechania & Sitaraman, 2024).

3. The Agentic Innovation Economics Model

3.1 Economic Environment

We consider a continuous-time economy with three sectors:

- Final Goods Sector: produces output Y using technology stock K and labour L.

- Human R&D Sector: employs human researchers H to expand the knowledge stock through Exploiting and Expanding discovery (following the capability hierarchy of Haefner et al. (2021)).

- Agentic R&D Sector: deploys a population of AI agents A to explore the technological possibility space autonomously (the Exploring capability level).

Assumption 1 (Factor Markets). All factor markets are competitive. The total workforce \bar{L} is fixed, with H + L = \bar{L}. Agents A are non-rival and can be replicated at marginal cost c per agent-period. The knowledge stock K is non-rival and partially excludable through patents.

Assumption 2 (Agent Capabilities). AI agents are capable of: (i) exploring the technological possibility space in parallel (simultaneous multi-directional search); (ii) building on each other’s discoveries through AI-to-AI knowledge transfer at negligible marginal cost; and (iii) self-improving their discovery productivity through recursive optimisation. These capabilities generate a superlinear relationship between the number of agents and aggregate agentic innovation output, consistent with the empirical scaling laws documented for large language models (Besiroglu et al., 2024).

Assumption 3 (Human–Agent Coexistence). Human researchers and AI agents are technological complements at the level of the innovation system, even where they substitute at the task level (Arsenyan et al., 2023). Human researchers provide objective-setting, ethical evaluation, and contextual judgment that AI agents cannot currently replicate; AI agents provide scalable exploration capacity that human researchers cannot match. The two-sector structure reflects this functional complementarity.

3.2 Knowledge Accumulation

Definition 1 Definition 1 (Hybrid Knowledge Dynamics). The rate of change of the aggregate knowledge stock K is governed by the hybrid knowledge dynamics equation:

\dot{K} = \phi_H H + \phi_A A^{\gamma} K^{\phi}, \tag{1}

where \phi_H > 0 is human innovation productivity, \phi_A > 0 is the agentic innovation productivity coefficient, \gamma \geq 1 captures the superlinear scaling of agentic exploration, and \phi \in [0, 1) captures the dependence of new discoveries on the existing knowledge stock (knowledge complementarity in the agentic process, analogous to the “standing on shoulders” effect of Romer (1990)).

Remark. For A = 0, Equation 1 reduces to the linear human innovation term \phi_H H, recovering a limiting case analogous to Jones’s (1995) semi-endogenous model when the knowledge stock is normalised to 1. For H = 0, the model yields a pure agentic growth path, where K grows as a power function of A and K itself. The hybrid specification nests both extremes and generates a continuum of growth regimes parameterised by the agentic share of R&D. This structural flexibility is consistent with the empirical diversity of AI adoption patterns documented by Bahoo et al. (2023) across corporate innovation contexts.

3.3 Innovation Production Function

Following the broader R&D-based growth literature, we specify a gross innovation output function I that maps total R&D inputs to the flow of new ideas:

I(H, A) = \alpha H^{\beta} + \delta A^{\eta}, \tag{2}

where \alpha, \delta > 0 are productivity parameters and \beta, \eta \in (0,1] are output elasticities. We impose:

Assumption 4 (Differential Productivity). \eta > \beta: the marginal innovation productivity of AI agents exceeds that of human researchers in the neighbourhood of the steady state, for sufficiently large A and sufficiently low compute cost c.

Assumption 4 encodes the key AIE hypothesis: at scale, agentic exploration of the idea space outpaces human discovery, consistent with the empirical finding by Besiroglu et al. (2024) that deep learning capital deepening in R&D may double US growth rates, and with the capability hierarchy evidence of Haefner et al. (2021).

Remark. The additive separability of Equation 2 has both virtues and limitations. It implies that human and agentic inputs are independent (neither perfect complements nor substitutes in the innovation flow), capturing the functional coexistence argument of Arsenyan et al. (2023) at the system level while acknowledging task-level substitution. Extensions with multiplicative or CES structures would allow richer complementarity patterns and are an important direction for future work.

3.4 Final Goods Production

Output is produced using a Cobb-Douglas technology:

Y = K^{\theta} L^{1-\theta}, \quad \theta \in (0,1), \tag{3}

where K represents the accumulated technology stock (rather than physical capital, following the Romer (1990) tradition in which ideas enter production directly through variety). Since \dot{K} > 0 from Equation 1, output growth follows as:

g_Y = \theta g_K + (1-\theta) g_L. \tag{4}

With g_L = n (exogenous population growth rate), the long-run growth rate of per capita output is g_y = g_Y - n = \theta g_K.

3.5 Balanced Growth Path

We characterise the model’s BGP, defined as a trajectory along which g_K is constant and positive.

Proposition 1 Proposition 1 (BGP under Pure Human Innovation). In the absence of agentic R&D (A = 0), the BGP knowledge growth rate is:

g_K^H = \frac{\phi_H H^*}{K^*}, \tag{5}

which is bounded above by \phi_H \bar{L} and converges to a stationary value proportional to the share of the workforce in R&D. Per capita output growth equals \theta g_K^H.

Proof. Along the BGP, \dot{K}/K = \phi_H H/K = \text{constant}, implying H and K grow at the same rate. Since H \leq \bar{L} is bounded, g_K^H is bounded. The allocation H^* is determined by the research arbitrage condition (see Appendix Section 13.1).

Proposition 2 Proposition 2 (BGP under Hybrid Innovation). In the full hybrid model with both human and agentic R&D, define \rho \equiv \phi_A A^{\gamma} K^{\phi} / (\phi_H H) as the agentic innovation ratio. The BGP knowledge growth rate satisfies:

g_K^{HA} = g_K^H \cdot (1 + \rho), \tag{6}

so that g_K^{HA} > g_K^H whenever A > 0. Furthermore, g_K^{HA} is increasing in A, \phi_A, \gamma, and \phi.

Proof. From Equation 1, \dot{K}/K = \phi_H H/K + \phi_A A^{\gamma} K^{\phi-1}. On the BGP where \dot{K}/K is constant, this requires A^{\gamma} K^{\phi-1} to be constant, which holds if g_K^{HA} = \gamma g_A / (1-\phi). Substituting and using the definition of \rho gives Equation 6. See Appendix Section 13.2 for the full derivation.

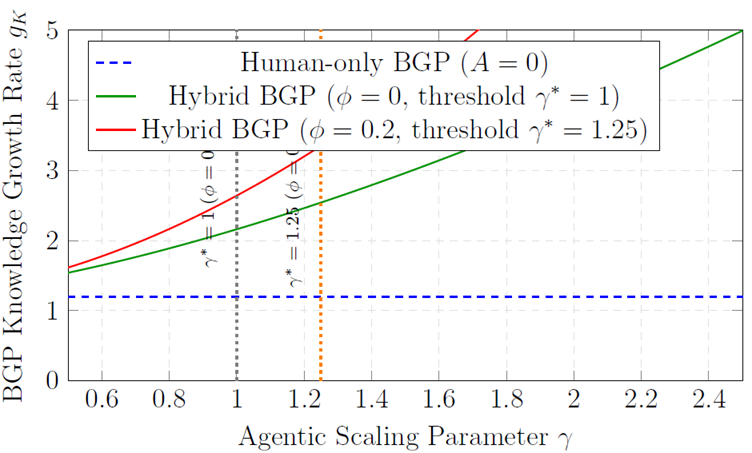

Theorem 1 Theorem 1 (Supra-Romer Growth Regime). If \gamma > 1/(1-\phi), the hybrid model exhibits an accelerating BGP: the knowledge growth rate g_K^{HA}(t) is strictly increasing in time along the balanced trajectory, implying a permanent acceleration of per capita output growth. In the limiting case \phi \to 0, this condition reduces to \gamma > 1, and the model generates a Type~I growth singularity in the sense of Aghion et al. (2019): the time to each successive doubling of K decreases without bound.

Proof. Differentiating g_K^{HA} with respect to time and using \dot{K} = g_K K, the condition for \partial g_K^{HA}/\partial t > 0 reduces to \gamma(1-\phi) > 1, i.e. \gamma > 1/(1-\phi). When \phi \to 0, this simplifies to \gamma > 1. The singularity result follows from the argument in Aghion et al. (2019): if g_K is increasing and unbounded, the time integral of g_K diverges, implying K \to \infty in finite time under the additional regularity condition that g_K grows at least as fast as a positive power of itself.

Remark. Theorem Theorem 1 makes explicit the conditions under which agentic AI may, in principle, deliver explosive growth. Critically, the singularity does not require full automation of human tasks—only superlinear scaling (\gamma > 1/(1-\phi)) in the agentic R&D sector. This contrasts with the full-automation condition of Aghion et al. (2019), making the AIE singularity threshold potentially more attainable under near-term technological conditions. The threshold is also consistent with the three-level capability framework of Haefner et al. (2021): the Exploring level of AI capability corresponds precisely to the regime where \gamma begins to exceed the critical threshold.

Figure Figure 1 illustrates the relationship between agentic scaling and knowledge growth along the BGP.

4. Firm-Level Model: Optimal Innovation Investment

4.1 The Firm’s Problem

Consider a representative R&D-intensive firm that maximises profit by choosing the optimal mix of human researchers H and AI agents A:

\max_{H, A \geq 0} \quad \Pi = P \cdot I(H, A) - wH - cA, \tag{7}

where P > 0 is the market value of an innovation (proportional to the present value of monopoly rents under a standard Dixit-Stiglitz pricing structure), w is the researcher wage, and c is the per-agent compute cost. Using the innovation production function Equation 2:

\Pi = P\bigl(\alpha H^{\beta} + \delta A^{\eta}\bigr) - wH - cA. \tag{8}

4.2 Optimal Input Conditions

First-order conditions yield:

\frac{\partial \Pi}{\partial H} = P \alpha \beta H^{\beta-1} - w = 0 \quad \implies \quad H^* = \left(\frac{P\alpha\beta}{w}\right)^{1/(1-\beta)}, \tag{9}

\frac{\partial \Pi}{\partial A} = P \delta \eta A^{\eta-1} - c = 0 \quad \implies \quad A^* = \left(\frac{P\delta\eta}{c}\right)^{1/(1-\eta)}. \tag{10}

The optimal innovation input mix is therefore fully separable: each factor is chosen independently by equating its marginal revenue product to its cost. The relative intensity of AI-versus-human R&D depends critically on the ratio c/w—the relative price of compute versus human capital.

Proposition 3 Proposition 3 (Substitution and Complementarity). Define the agent intensity ratio \rho^* \equiv A^*/H^*:

\rho^* = \left(\frac{P\delta\eta}{c}\right)^{1/(1-\eta)} \bigg/ \left(\frac{P\alpha\beta}{w}\right)^{1/(1-\beta)}. \tag{11}

Under Assumption 4 (\eta > \beta):

- \partial \rho^*/\partial c < 0: falling compute cost monotonically increases agent intensity.

- \partial \rho^*/\partial w > 0: rising researcher wages accelerate the substitution toward agentic R&D.

- There exists a critical compute cost \bar{c} such that for all c < \bar{c}, the interior optimum H^*, A^* > 0 remains valid, but as c \to 0, the firm’s optimal allocation concentrates arbitrarily large A^* relative to H^*, effectively specialising in agentic R&D for exploratory tasks while retaining a positive (but relatively shrinking) stock of human researchers for objective-setting and evaluation functions that AI agents cannot yet perform.

Proof. Parts (i) and (ii) follow directly from differentiation of Equation 11. For part (iii): from Equation 9, H^* = (P\alpha\beta/w)^{1/(1-\beta)} is independent of c, so H^* remains strictly positive for all finite w. From Equation 10, A^* = (P\delta\eta/c)^{1/(1-\eta)} \to \infty as c \to 0 (since 1/(1-\eta) > 0). Hence \rho^* \to \infty as c \to 0, confirming effective specialisation in agentic R&D. Note: the economic corner solution (where H^* = 0 is literally chosen) requires non-separability or budget constraints not present in the unconstrained model; under Assumptions 2 and 3, human researchers retain positive value for governance and objective-setting functions even when c \to 0.

Remark. This result aligns with the empirical evidence in Bone et al. (2025), who document that AI adoption increases the relative demand for human workers with AI-complementary skills (agentic supervisors, AI evaluators, prompt engineers) even as it reduces demand for workers in directly substituted tasks. As compute costs continue to decline at Moore’s-law rates (historically \approx 30–50\% per year for GPU throughput per dollar), R&D-intensive firms will progressively concentrate human researchers on the higher-order oversight tasks identified by Haefner et al. (2021)’s Exploring capability level, while delegating routine hypothesis search to AI agents.

4.3 Dynamic Investment Problem

To capture intertemporal dynamics, we extend the static model to a continuous-time firm problem where the knowledge stock accumulated by the firm, k(t), evolves as:

\dot{k} = I(H, A) - \lambda k, \tag{12}

where \lambda > 0 is the depreciation rate of firm-level knowledge (reflecting obsolescence from competitors’ innovations). The firm maximises:

V = \int_0^{\infty} e^{-r t} \bigl[P \cdot k(t) - wH(t) - cA(t)\bigr] dt, \tag{13}

subject to Equation 12. Using the current-value Hamiltonian, the optimal trajectories H^*(t) and A^*(t) satisfy:

H^*(t) = \left(\frac{q(t)\,\alpha\beta}{w}\right)^{1/(1-\beta)}, \qquad A^*(t) = \left(\frac{q(t)\,\delta\eta}{c}\right)^{1/(1-\eta)}, \tag{14}

where q(t) is the costate variable (shadow value of firm knowledge), evolving as \dot{q} = (r+\lambda)q - P. Along the steady state, q^* = P/(r+\lambda), recovering the static solution Equation 9–Equation 10 with P replaced by its discounted present value.

Remark. The dynamic model reveals that the transition to agentic R&D dominance is driven not only by the level of compute costs but by their rate of decline. A firm anticipating rapid cost reductions will optimally front-load agentic R&D investment, consistent with the observed pattern of large-scale AI infrastructure build-outs by leading technology firms (Vipra & Korinek, 2024). The responsible AI literature (Dai et al., 2026) highlights that this transition also accelerates governance challenges: as agentic R&D scales, the risks of misalignment, data security failures, and reduced human cognitive engagement in knowledge creation intensify.

5. Market Structure: Compute Capital and Winner-Take-Most Dynamics

5.1 Computational Capital as the New Strategic Factor

In the human-innovation economy, the strategic scarcity was human capital: firms competed for researchers, university talent pipelines determined R&D capacity, and the distribution of human capital bounded inequality in innovation output. AIE introduces a new strategic factor: computational capital C—the stock of GPUs, specialised chips, data-centre infrastructure, and the trained model weights residing on them—which determines the number and capability of deployable AI agents.

Define A = f(C) with f' > 0 and f'' < 0 (concave production of agents from compute), so that firm-level innovation becomes:

I_i = \alpha H_i^{\beta} + \delta [f(C_i)]^{\eta}. \tag{15}

Firms with larger compute endowments C_i produce more innovation, and since \eta > \beta (Assumption 4), the marginal return to compute investment eventually dominates the marginal return to human capital investment when f(C) \geq (w/c)^{1/(\eta-\beta)} \cdot (\alpha\beta/\delta\eta)^{1/(\eta-\beta)}.

5.2 Compute Concentration and Innovation Inequality

Proposition 4 Proposition 4 (Winner-Take-Most in Agentic Innovation). Suppose the compute-production function f(C) exhibits decreasing returns (f'' < 0) and the compute market is characterised by increasing returns to scale in training (fixed costs of frontier-model training are convex in target capability). Then:

- The Nash equilibrium in the compute investment game is one of extreme concentration, with a small number of firms holding a disproportionate share of total compute C_{\text{total}};

- The Gini coefficient of innovation output across firms increases with \eta (the AI productivity elasticity) and decreases with c (the compute price);

- As c \to 0, the innovation output distribution converges to a degenerate distribution concentrated at the largest-compute firm.

Proof. The proof combines the theory of supermodular games (Milgrom & Roberts, 1990) with the observation that the return to incremental compute is supermodular in total compute: large-C firms benefit disproportionately from additional compute due to their larger trained model base. Formally, define the effective cost function as \tilde{c}(C_i) = cC_i - \kappa C_i^{\mu}, \mu > 1, for firms above a minimum viable compute threshold. The Nash equilibrium exhibits strategic complementarities in the sense that unilateral increase in C_i raises the marginal return to C_j for all j \neq i (through the competitive pressure channel). The resulting concentration result and parts (ii)–(iii) follow from Lorenz dominance of the concentrated over the uniform compute distribution in generating innovation output. See Appendix Section 13.3 for the full argument.

This proposition provides the theoretical grounding for the empirical findings of Babina et al. (2024), who document that AI-powered growth concentrates among ex-ante larger firms, and Vipra & Korinek (2024), who show that the GPU market is dominated by a single firm with \approx 90\% market share. Rikap (2024) document the same mechanism in the longer history of ICT innovation, where early data and model advantages create self-reinforcing intellectual monopolisation. The market data of Ante (2026) corroborate this concentration mechanism at the ecosystem level: in the DeFi AI agent market, Meme & Sentiment agents command 59.4% of total market capitalisation ($5.10 billion of $8.6 billion total), reflecting the winner-take-most dynamics predicted by Proposition Proposition 4 when cultural attention rather than computational output is the scarce resource.

5.3 Schumpeterian Dynamics under Agent Competition

The AIE framework modifies Schumpeterian creative destruction in an important way. In the standard quality-ladder model (Aghion & Howitt, 1992), each new innovation triggers entry by a new monopolist who displaces the incumbent. Under agentic innovation, the incumbent firm can deploy its AI agents to continuously improve existing products and explore new product spaces simultaneously, at a rate proportional to its compute stock. This generates inside-the-firm creative destruction: the largest-compute firm not only dominates current production but also monopolises the exploration of adjacent innovation spaces, pre-empting entry by smaller competitors.

Remark. This mechanism—combine scale, data, and compute to monopolise both incumbent markets and adjacent innovation frontiers—is precisely what Rikap (2024) identify empirically as the defining feature of “intellectual monopolies” among Big Tech firms, and what K. G. Huang et al. (2025) identify as the strategic synthesis level of their breakthrough innovation pyramid, accessible only to firms with sufficient platform infrastructure to integrate trading and exploration across multiple innovation frontiers.

6. Labour Market Implications

6.1 Testable Propositions on R&D Labour Demand

Combining the firm-level and macroeconomic models, we derive four testable propositions that map directly to observable data.

Proposition 5 Proposition 5 (Positive Innovation Output Effect). Firms increasing their AI agent stock A by \Delta A experience a proportional increase in innovation output I equal to \delta \eta [A + \Delta A]^{\eta} - \delta\eta A^{\eta} \approx \delta\eta^2 A^{\eta-1} \Delta A for small \Delta A. Because \eta < 1, this is concave in A—declining marginal returns—but positive throughout, implying that every marginal investment in AI agents generates measurable innovation output.

Empirical prediction: A one-standard-deviation increase in firm-level AI investment is associated with statistically significant increases in patents, trademarks, and new product launches.

Evidence: Babina et al. (2024) find that a one-standard-deviation increase in AI investment is associated with a 13% increase in trademarks and a 24% increase in product patents, consistent with this prediction. Truong & Papagiannidis (2022) document that AI enables innovation at all four stages of the pipeline, confirming broad-spectrum innovation output effects.

Proposition 6 Proposition 6 (Non-Monotone R&D Employment Effect). The total demand for human researchers at the firm level is H^* = (P\alpha\beta/w)^{1/(1-\beta)}, which is independent of A in the static model (the innovation production function is additively separable). However, through the competition-for-market-share channel, AI-driven growth concentrates innovation output in large-C firms, reducing the optimal size of the research workforce at firms with lower compute endowments.

Empirical prediction: Aggregate R&D employment is ambiguous; high-AI-investment firms may hire more AI-complementary researchers (system designers, prompt engineers, evaluators) while displacing pure exploratory researchers in lower-C firms.

Evidence: Acemoglu & Restrepo (2019) document that automation technologies reduce labour demand in directly affected tasks but generate new task creation. Babina et al. (2024) find that AI investment is associated with employment growth among publicly traded (high-C) firms, with muted or negative effects at non-publicly-traded firms. The skill-based hiring data of Bone et al. (2025) confirm that AI role demand grew 21% over 2018–2023 while degree requirements for these roles declined 15%, consistent with increasing demand for AI-complementary competencies over credentials. L. Huang et al. (2025) further document that AI adoption augments human and structural capital in the medium run, with human cognitive functions retaining primacy at the creative frontier.

Proposition 7 Proposition 7 (Labour Share Decline under Agentic Innovation). As compute cost c falls and A^* rises relative to H^*, the labour income share in the R&D sector—defined as s_L = wH^* / (wH^* + cA^*)—falls monotonically. Formally:

\frac{\partial s_L}{\partial c} = \frac{wH^*}{(wH^* + cA^*)^2} \left[A^* + c\frac{\partial A^*}{\partial c}\right]. \tag{16}

Since \partial A^*/\partial c = -\frac{1}{(1-\eta)c} A^* < 0, we have A^* + c(\partial A^*/\partial c) = A^*\bigl[1 - \tfrac{1}{1-\eta}\bigr] = -\tfrac{\eta}{1-\eta} A^* < 0. Therefore \partial s_L / \partial c < 0, confirming that s_L is decreasing in c: as compute costs fall, the labour income share in the R&D sector falls.

Evidence: Lowitzsch et al. (2024) document a long-run trend of declining labour income shares associated with capital-intensive automation, which AIE predicts will accelerate as compute costs continue their historical decline.

Proposition 8 Proposition 8 (Growth Acceleration from Agent Scaling). Under the calibration \gamma > 1/(1-\phi) from Theorem Theorem 1, a doubling of the aggregate AI agent population A increases the BGP knowledge growth rate by a factor exceeding 2^{1/(1-\phi)}. For \phi = 0 and \gamma = 1.5 (a moderate estimate consistent with the observed scaling laws for large language models (Besiroglu et al., 2024)), this implies a 2^{1.5} \approx 2.83-fold increase in g_K per doubling of agents.

Evidence: Besiroglu et al. (2024) find that if deep learning diffuses widely across R&D, the US economic growth rate may double, consistent with \gamma \approx 1.3–1.6 in our framework. K. G. Huang et al. (2025) document breakthrough innovation rate acceleration consistent with Proposition Proposition 8 in sectors where AI has been deployed at scale.

6.2 Skilled Labour Complementarity and the Agentic Supervisor Role

An important qualification to the substitution narrative is that agentic innovation is complementary to a specific class of human labour—what we term agentic supervisors: individuals capable of defining objective functions for agents, evaluating emergent innovations for feasibility and market fit, integrating agent-generated discoveries into product pipelines, and providing the ethical constraints that prevent unbounded algorithmic exploration from generating harmful outputs (Dai et al., 2026).

This complementarity creates a bifurcated labour market: demand rises for highly skilled agentic supervisors (with premium wages) while demand falls for routine exploratory R&D labour, deepening the polarisation dynamic documented by Acemoglu & Restrepo (2019) in the broader automation context. The empirical evidence of Bone et al. (2025)—showing a 23% AI skills wage premium and 21% growth in AI role demand alongside 15% declining degree requirements—captures precisely this bifurcation: it is not the credential (degree) that commands premium wages, but the practical AI-complementary skill set of the agentic supervisor.

The boundary between agentic and human innovation capability lies, as L. Huang et al. (2025) document, at the level of cognition and creativity. AI systems are currently “semi-cognitive”: they excel at pattern recognition, recombination, and structured hypothesis generation, but they lack the contextual judgment, ethical reasoning, and genuine creativity that define the highest-level agentic supervisor functions. This implies that human–agent coexistence (Arsenyan et al., 2023) will persist as the dominant organisational structure for R&D well into the foreseeable future, even as the balance of exploratory work shifts toward agentic systems.

7. Governance Implications

7.1 The Compute Monopoly Problem

Proposition Proposition 4 predicts that, absent intervention, agentic innovation converges to winner-take-most dynamics driven by compute concentration. This is not merely a distributional concern: monopolisation of the agentic innovation sector suppresses the variety and direction of exploration, potentially locking the economy into a narrow set of technological trajectories determined by the preferences of a small number of compute-owning firms. Vipra & Korinek (2024) characterise this risk as “concentrating intelligence,” documenting that the GPU market, foundation model training, and AI-as-a-service provision are all structured as natural monopoly or oligopoly. The DeFi evidence of Ante (2026) corroborates this concern at the ecosystem level: even in ostensibly decentralised environments, AI agent governance tends to re-centralise around compute-rich actors absent countervailing institutional design.

The policy response is threefold:

(i) Compute infrastructure as public utility. Drawing on the public-option literature (Narechania & Sitaraman, 2024), governments should establish national AI research computing resources (analogous to the US NAIRR proposal) providing open access to sufficient compute for academic and small-firm R&D. A concrete target suggested by our model: public compute access sufficient to maintain at least 10% of aggregate A outside the top-3 compute-owning firms, preventing the degenerate concentration predicted by Proposition Proposition 4(iii).

(ii) Data commons governance. Since agentic systems depend on large training datasets, and since data exhibits similar network externalities to compute, governance frameworks must address data hoarding and ensure that publicly funded data is accessible for agentic R&D (G7 Open Future Initiative, 2024; Jones & Tonetti, 2020). The responsible AI framework of Dai et al. (2026) recommends a multi-level governance structure addressing data security, privacy, and misinformation risks simultaneously, ensuring that responsible knowledge creation principles are embedded at the infrastructure level.

(iii) Open innovation mandates. Compulsory licensing of frontier model weights for non-commercial research applications, reducing barriers to entry in the agentic innovation ecosystem, counteracts the inside-the-firm creative destruction dynamic identified in Section 6.

7.2 Responsible AI in Knowledge Creation

The transition to agentic innovation raises governance challenges that go beyond compute concentration to the quality and integrity of the knowledge produced. Dai et al. (2026) identify four critical risks of generative and agentic AI in knowledge creation: data security failures, privacy violations, misinformation propagation, and reduced human cognitive engagement in the knowledge creation process. These risks manifest specifically within the SECI knowledge creation framework (Nonaka & Takeuchi, 1995): agentic AI affects all four knowledge conversion phases (Socialisation, Externalisation, Combination, Internalisation), but does so in ways that may undermine the tacit-knowledge foundations of genuine innovation if human cognitive engagement is systematically reduced.

The AIE framework formalises this concern: if agentic innovation displaces human researchers to the extent that H^* \to 0, the model predicts growth acceleration (via Theorem Theorem 1) but also a loss of the human-mediated knowledge validation and ethical filtering that prevents harmful innovations from entering the production pipeline. A welfare-maximising innovation policy must therefore target not just the growth rate but the quality-adjusted knowledge accumulation rate, incorporating the responsible AI principles identified by Dai et al. (2026) as constraints on the objective function rather than ex post regulatory add-ons.

7.3 Decentralised Autonomous Innovation Governance

An emerging institutional response to compute concentration and governance centralisation is the decentralised autonomous organisation (DAO). DAOs operating via blockchain smart contracts and token-based governance provide a potential alternative organisational form for agentic R&D that does not require centralised compute ownership (Ante, 2026; Santana & Albareda, 2022). Santana & Albareda (2022) identify three DAO governance principles—decentralisation, automation, and autonomy—and four theoretical lenses (transaction cost theory, collective action theory, agency theory, and sociomateriality) through which DAO governance can be evaluated. Applied to the AIE context, DAO governance for agentic R&D offers:

- Distributed compute pooling: token holders contribute compute resources to a shared agentic R&D pool, counteracting the concentration dynamics of Proposition Proposition 4.

- Collective objective-setting: governance token votes determine the exploration targets of the agentic R&D system, preventing single-firm lock-in of innovation direction.

- Transparent innovation accounting: smart-contract execution provides immutable records of agentic R&D activities, addressing the opacity risks identified by Ante (2026) and the accountability requirements of Dai et al. (2026).

Ante (2026) document that as of December 2024, 306 AI agents operating in DeFi ecosystems aggregate to $8.6 billion in market capitalisation, demonstrating that DAO-based agentic innovation is already a functioning, economically significant institutional form. Integrating DAO governance principles into the AIE framework suggests a hybrid institutional architecture: proprietary agentic R&D for product innovation (under the patent regime recommended in Section 8.4) coexisting with DAO-governed agentic exploration of public-good knowledge frontiers (open-access genomics, climate modelling, materials discovery) funded through public compute infrastructure and governed by collective token mechanisms.

7.4 Knowledge Ownership in the Agentic Economy

The AIE model raises a fundamental question that classical intellectual property theory cannot resolve: who owns AI-generated innovations? Under the Romer (1990) framework, the innovating entrepreneur secures a patent and earns temporary monopoly rents, with the innovation eventually entering the public knowledge stock. Under agentic innovation, the “innovator” is an AI system owned by the compute-capital holder. This creates a potential unlimited appropriation of rents by compute owners, with no corresponding mechanism for knowledge to flow into the public domain.

Three institutional responses are possible:

(i) Firm ownership: AI-generated innovations are owned by the deploying firm. This maximises innovation incentives but concentrates rents at compute-capital holders, exacerbating inequality consistent with Proposition Proposition 7.

(ii) AI developer ownership: innovations belong to the firm that trained the underlying AI system. This creates a vertical monopoly over the entire innovation stack, potentially more concentrated than case (i).

(iii) Public commons: AI-generated innovations enter the public domain, funded through compute taxation or Pigouvian innovation subsidies. This maximises knowledge diffusion but may reduce private investment incentives.

We argue that a mixed regime—short-duration patents for AI-generated innovations (3–5 years rather than 20) combined with compulsory licensing, a public domain transition, and a portion of agentic innovation rents directed to a public compute infrastructure fund—best balances the innovation incentive and diffusion effects identified in our model.

7.5 Algorithmic Accountability and Innovation Governance

Beyond ownership, agentic innovation raises novel accountability challenges. Innovations generated by autonomous agents may be non-interpretable, potentially harmful, or strategically misaligned. These risks require an agentic innovation governance framework with three components:

(i) Objective function auditing. Regulators should have access to the objective functions governing agentic R&D systems. The EU Artificial Intelligence Act (2024) establishes a risk-based compliance framework for high-risk AI systems, requiring conformity assessments, transparency obligations, and human oversight mechanisms for AI deployed in high-stakes domains. Applied to agentic R&D, this framework implies that AI agents conducting innovation in high-consequence domains (pharmaceutical discovery, materials for weapons, autonomous system design) should be subject to conformity assessments and mandatory human oversight gating.

(ii) Human-in-the-loop requirements. Consistent with the responsible AI principles of Dai et al. (2026) and the coexistence framework of Arsenyan et al. (2023), high-consequence innovation domains should require human review at defined decision gates, preventing purely agent-driven deployment of potentially harmful discoveries.

(iii) Open-access research platforms. The governance framework should distinguish between closed (proprietary) and open (academically accessible) agentic R&D infrastructure, with regulatory requirements calibrated to the risk profile and public-good character of the innovation domain, drawing on the DAO governance architecture described above.

8. Potential Empirical Applications

The four propositions of Section 7 generate testable predictions that future empirical work can evaluate. We identify four primary research designs.

(1) Firm-Level Panel Studies. The approach of Babina et al. (2024)—using resume data and job postings to measure firm-level AI investment—can be extended to measure specifically the deployment of agentic systems (autonomous agents, multi-agent pipelines, AI Scientist-type workflows), distinguished from narrow ML tools. The AIE model predicts that agentic investment will be associated with disproportionately higher product innovation (Proposition Proposition 5), larger employment effects concentrated at high-compute firms (Proposition Proposition 6), and declining R&D labour income shares (Proposition Proposition 7). The skill-based hiring methodology of Bone et al. (2025) provides a natural extension: tracking the composition of AI-related job postings over time would allow identification of the agentic supervisor role’s emergence and wage premium trajectory.

(2) Cross-Country Growth Accounting. Drawing on the framework of Besiroglu et al. (2024), one can construct cross-country estimates of \gamma—the agentic scaling parameter—using data on compute investment, AI patent applications, and R&D productivity from the OECD AI Policy Observatory and WIPO patent databases. Proposition Proposition 8 predicts that countries with higher compute per researcher will exhibit higher g_K growth rates, controlling for human capital and institutional quality. The cross-sector framework of Bahoo et al. (2023) provides the research-stream taxonomy needed to categorise innovation outputs across the eight corporate AI application domains they identify.

(3) Sector-Level Innovation Velocity. In sectors where agentic R&D has been deployed at scale (protein folding with AlphaFold, materials discovery with GNoME, drug target identification with AI systems), innovation velocity—measured as the rate of new patent filings, scientific publications, or new product approvals—should exhibit the acceleration predicted by Proposition Proposition 8. Calibrating these sector-level estimates allows identification of \gamma and \phi from Equation 1. The breakthrough innovation framework of K. G. Huang et al. (2025) provides the conceptual structure for distinguishing incremental from breakthrough innovations in these velocity measures.

(4) DeFi Agent Ecosystem Studies. The Ante (2026) dataset of 306 AI agents with market capitalisation, governance, and community metrics provides a natural laboratory for testing AIE’s market structure predictions. Specifically: the winner-take-most prediction of Proposition Proposition 4 can be tested by examining the Gini coefficient of market capitalisation across agent categories over time; the governance transition prediction can be examined by tracking the autonomy-decentralisation quadrant positions of agents as the market matures; and the labour complementarity prediction can be tested by examining how agent ecosystem growth affects demand for human oversight roles in DeFi organisations.

9. Limitations and Future Research

The present framework involves several simplifications that future research should relax.

Agent heterogeneity. We treat AI agents as homogeneous, abstracting from the diversity of agent capabilities, architectures, and objective functions that characterises real-world deployment. The typology of Ante (2026)—distinguishing Trading & Analytics agents from Development, Sentiment, and Entertainment agents—suggests that a heterogeneous-agent extension would generate richer predictions about inter-sector knowledge spillovers and the composition of the innovation output mix.

Stochastic innovation arrivals. Our dynamic firm model is deterministic; introducing stochastic innovation arrival (as in the quality-ladder literature (Aghion & Howitt, 1992)) would generate more realistic distributions of firm size, innovation output, and compute investment. This extension would also enable welfare comparisons under different governance regimes, allowing quantification of the efficiency loss from compute concentration relative to the socially optimal agentic R&D allocation.

Open-source versus proprietary dynamics. We have not modelled the two-sided interaction between the open-source and proprietary agentic R&D sectors, a frontier that Gans (2025) identifies as crucial for understanding AI’s long-run growth implications. The DAO governance structure discussed in Section 8 represents an institutional bridge between these sectors, and modelling the equilibrium dynamics of this interface is an important direction for future work.

Responsible AI constraints. The current model treats the innovation production function as unconstrainedly maximised subject to cost. Introducing responsible AI constraints—minimum human-in-the-loop requirements, maximum allowable exploration-domain scope without human validation, data governance compliance costs—as formal constraints on the optimisation programme would allow welfare analysis of governance policy design (Dai et al., 2026).

Human–agent coexistence dynamics. The model’s additive separability of I(H,A) does not capture the time-varying complementarity between human and agentic R&D identified by Arsenyan et al. (2023) and L. Huang et al. (2025). A multiplier structure, in which human cognitive engagement enhances the quality of agentic exploration, would generate richer predictions about the optimal human–agent ratio trajectory as AI capabilities develop toward higher levels of the Haefner et al. (2021) information-processing hierarchy.

10. Conclusion

This paper has introduced Agentic Innovation Economics (AIE) as a formal extension of endogenous growth theory to the era of autonomous AI agents. Our four principal contributions are:

(1) The Hybrid Knowledge Dynamics Equation (Equation 1): a specification that integrates human and agentic innovation into a unified knowledge accumulation framework, generating a family of balanced growth paths parameterised by the agentic scaling exponent \gamma and the knowledge-stock complementarity coefficient \phi. The equation nests the Romer–Jones tradition while extending it to capture the superlinear scaling properties of agentic exploration systems, consistent with the information-processing hierarchy of Haefner et al. (2021) and the GPT-based growth literature (Brynjolfsson et al., 2021; Truong & Papagiannidis, 2022).

(2) The Supra-Romer Theorem (Theorem Theorem 1): a precise characterisation of the parametric conditions (\gamma > 1/(1-\phi)) under which agentic innovation generates permanently accelerating growth—a technological regime change comparable in its implications to the Industrial Revolution. This threshold is more attainable than the full-automation condition of Aghion et al. (2019) and provides a concrete forecasting target for the agentic AI scaling literature.

(3) Winner-Take-Most Dynamics (Proposition Proposition 4): a formal account of how compute-capital concentration translates, through the agentic innovation production function, into extreme concentration of innovation output—with profound implications for market structure, labour income shares, and knowledge governance. The empirical evidence of Ante (2026), Babina et al. (2024), and Vipra & Korinek (2024) consistently supports this prediction.

(4) An Integrated Governance Architecture: combining compute infrastructure policy, responsible AI in knowledge creation (Dai et al., 2026), DAO-based decentralised innovation governance (Ante, 2026; Santana & Albareda, 2022), and a mixed intellectual property regime. The governance architecture is grounded in the model’s welfare implications rather than being a descriptive addendum.

Four testable propositions link these theoretical results to the emerging empirical literature, providing a research agenda for the economics of autonomous AI. The labour market evidence of Bone et al. (2025) and L. Huang et al. (2025) supports the human–agent complementarity thesis that qualifies the pure substitution narrative, while the corporate innovation evidence of Babina et al. (2024) and Bahoo et al. (2023) supports the positive innovation output effects.

The transition from human-bounded to agent-driven innovation represents, in the language of Schumpeter (1942), a fundamental change in the character of the entrepreneurial function. Whether this change constitutes creative destruction in the service of prosperity, or the concentration of economic power at a scale unprecedented since the industrial revolution, will depend on the governance frameworks societies build in the years ahead. Agentic Innovation Economics aims to provide the theoretical tools necessary for that challenge—including not just the growth-accelerating upside of agentic R&D, but the concentration, distributional, and responsible-AI dimensions that determine whether the social change that accompanies technological forecasting is shared broadly or captured narrowly.

References

Appendix A: Proofs

A.1 Proof of Proposition 1 (Human-Only BGP)

In the absence of agentic R&D, knowledge dynamics are \dot{K} = \phi_H H. Optimal allocation of the workforce between goods production and R&D is determined by the research arbitrage condition: the marginal product of a researcher equals the wage. In a symmetric equilibrium with Cobb-Douglas goods production Equation 3, the wage in goods production is w = (1-\theta) K^{\theta} L^{-\theta}, and the return to a researcher is r_R = \phi_H \cdot V_K, where V_K is the market value of a marginal unit of knowledge. Setting r_R = w and using the asset-pricing equation for knowledge under competitive product markets:

V_K = \frac{\theta K^{\theta-1} L^{1-\theta}}{r - g_K},

where r is the interest rate and g_K = \phi_H H/K on the BGP. Solving the fixed-point equation in H^*/\bar{L} yields the equilibrium R&D share and hence g_K^H. The upper bound \phi_H \bar{L} is achieved when all workers are researchers (L = 0), which violates goods-market feasibility; the interior solution requires \theta, (1-\theta) > 0, which holds by assumption.

A.2 Proof of Proposition 2 (Hybrid BGP)

On the BGP, both g_K and g_Y are constant. From Equation 1:

g_K = \frac{\phi_H H}{K} + \phi_A A^{\gamma} K^{\phi-1}.

For g_K to be constant when K is growing, the second term must be constant, requiring A^{\gamma} K^{\phi-1} to be constant. This holds if g_A / g_K = (1-\phi)/\gamma, i.e. g_A = g_K(1-\phi)/\gamma. Substituting and using \rho = \phi_A A^{\gamma} K^{\phi-1} / (\phi_H H/K):

g_K = \frac{\phi_H H}{K}(1 + \rho) = g_K^H (1 + \rho),

establishing Equation 6. The comparative statics follow from differentiating \rho with respect to A, \phi_A, \gamma, and \phi.

A.3 Proof of Proposition 4 (Winner-Take-Most)

Let N firms compete in compute investment, with firm i investing C_i and earning innovation output I_i = \alpha H_i^{\beta} + \delta [f(C_i)]^{\eta}. Suppose returns to compute are locally convex (fixed training costs create scale economies at the frontier), so that the effective cost function is \tilde{c}(C_i) = cC_i - \kappa C_i^{\mu}, \mu > 1, for firms above a minimum viable compute threshold \underline{C}.

Under supermodularity (Milgrom & Roberts, 1990), the Nash equilibrium of the compute investment game exhibits strategic complementarities in the sense that a unilateral increase in C_i raises the marginal return to C_j for all j \neq i (through the competitive pressure channel: incumbent monopolists invest more to deter entry). The resulting Nash equilibrium is one in which compute investment is concentrated at the largest-endowment firm, with all others investing at the minimum viable level. Parts (ii) and (iii) follow from the Lorenz dominance of the concentrated over the uniform compute distribution in generating innovation output, given \eta > 0.

A.4 Schumpeterian Extension: Quality Ladders with Agentic Exploration

Consider a quality-ladder extension in which each product line j has quality q_j(t) that jumps by factor \lambda > 1 upon innovation. Innovation in product line j by AI agents occurs at Poisson rate \mu_j = \phi_A A_j^{\gamma}, where A_j is the number of agents assigned to product j. The firm’s problem is to allocate A agents across J product lines to maximise the total value of innovations. Under isoelastic preferences, the optimal allocation assigns more agents to higher-quality lines (complementarity between quality and exploration productivity), generating the Zipf-like distribution of innovation rates across product lines observed empirically by Kogan et al. (2017). The growth rate of aggregate quality in this model is g_Q = \phi_A (\bar{A}/J)^{\gamma} \lambda, which is increasing in \gamma and in the aggregate agent deployment \bar{A}.